How Do Debit & Credit Card Transactions Work?

It’s important for all merchants — especially ecommerce businesses — to understand how typical credit and debit card transactions work.

There are many players that bring a transaction to fruition. Each of these services or components usually take a cut of your revenue. Businesses that want to audit and optimize these costs must understand how each entity works together to put funds where they need to go.

Further, when something goes wrong — a payment gateway fails, you get locked out of your merchant account, or you encounter a mysterious error code from your credit card processor — understanding how transactions work will help you resolve issues.

Knowing how each of these components work together (on both the customer and merchant side) will help you make informed decisions about what systems and services you implement in your business.

By the end of this post, you’ll understand:

- Who is Involved in Debit & Credit Transactions

- How Transactions Work

- How Refunds Work

- How Chargebacks Work

Who is Involved in Debit & Credit Transactions?

There are many services, softwares, organizations, and systems that work together to enable credit and debit card purchases. Here are the pieces working behind the scenes.

Cardholder

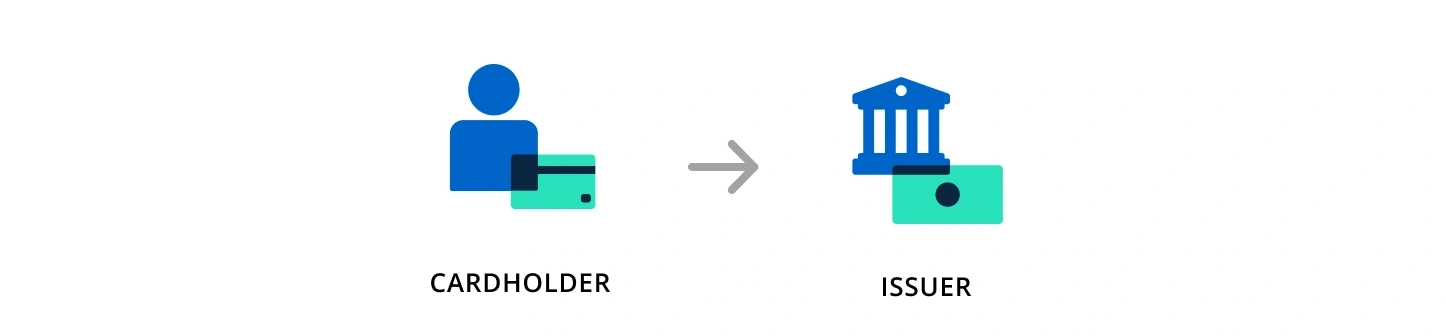

A cardholder is an individual who’s been authorized to make payments with a credit or debit card issued to them by an issuing bank.

Cardholders can initiate transactions and dispute charges, sometimes resulting in chargebacks.

Merchant

A merchant is a seller of goods or services that accepts payments from cardholders.

Merchants process payments and receive funds through a merchant account provided by an acquirer.

Card Brand

A card brand (sometimes called a card network or association) is an organization that facilitates payment card transactions.

It regulates who, where, and how cards are used. Examples of card brands include Visa®, Mastercard®, American Express®, Discover®, China UnionPay®, and JCB®.

Issuer

An issuer (or issuing bank) is the cardholder’s bank. These financial institutions issue payment cards and cardholder accounts to authorized consumers.

As a member of the card associations, issuing banks are authorized to issue payment cards on the associations’ behalf. Issuing banks act as liaisons so cardholders don’t have to deal with card associations and acquirers directly.

Acquirer

An acquirer (or acquiring bank) is a bank that provides merchant services. It is licensed to provide merchant accounts to qualified businesses, enabling those businesses to accept credit card payments.

Acquiring banks also acquire funds from the credit card issuer once a cardholder’s transaction has been approved.

Payment Processor

A payment processor shares and receives data from the card brands, acquirer, and gateway in order to process a merchant’s transactions.

Payment processors aren’t in network with card brands like acquirers and issuers are. However, a bit like a courier, they play a critical role in relaying data and funds back and forth between the merchant and cardholder banks.

Many payment processors will include compatible point-of-sale terminals for customers of their services.

Point-of-Sale Terminal

A point-of-sale (POS) terminal is a physical device or system used for receiving and processing payment card transactions.

Point-of-sale terminals are used almost exclusively for in-person transactions (as opposed to card-not-present transactions). They are one of the few cardholder-facing components of the transaction workflow.

Payment Gateway

The role of the payment gateway is to receive, protect, and safely share transaction information. It’s essentially a cash register for online sales but with more security features.

As opposed to POS terminals, payment gateways are most common in card-not-present (online) purchases.

CRM or Order Management System

A CRM (or customer relationship management) platform is a database that captures and organizes interactions with customers or potential customers. It also stores all relevant customer demographic information and purchase history.

Many CRMs offer integration with point-of-sale terminals or payment gateways to help merchants track their customers’ buying behaviors.

CRMs are not essential pieces of the transaction cycle — merchants can still accept and receive payments without them — but tracking customer behavior in a CRM is a best practice for effective businesses.

Chargeback Technology

As a business grows, it’s inevitable that chargeback activity will scale as well. Even with the strictest quality control mechanisms and the most generous refund policies, chargebacks happen.

It’s important to have a plan and system in place to handle these inevitable nuisances. Without a proactive strategy, the merchant could lose the ability to process payments.

Platforms like Kount can help. Kount’s technology makes it easy to prevent, analyze, and fight chargebacks.

How Transactions Work — An Example

If you’re confused by all these terms, you’re not alone! They’re a lot of similarly-named systems with only subtle differences.

As with most things, an example makes it easier to understand how debit and credit card processing works.

PHASE #1

Transaction

Let’s say Jason is in the market to buy a guitar. He decides to shop at Kat’s Music Shop for a used electric guitar. Kat has a guitar that strikes Jason’s fancy, and it’s only $200.

Jason pulls out his branded Visa credit card (issued to him by his issuing bank), enters the relevant information on the checkout page of Kat’s website, and clicks “Buy Now.”

Purchase

Jason’s simple act of initiating the transaction triggers a sequence of rapid, complex processes involving half a dozen different systems.

Next, the transaction immediately moves into the authorization phase.

PHASE #2

Authorization

Authorization is a conversation between a merchant and the issuing bank to determine if a transaction should be approved or declined. In this case, it’s Kat’s way of making sure Jason is good for the money.

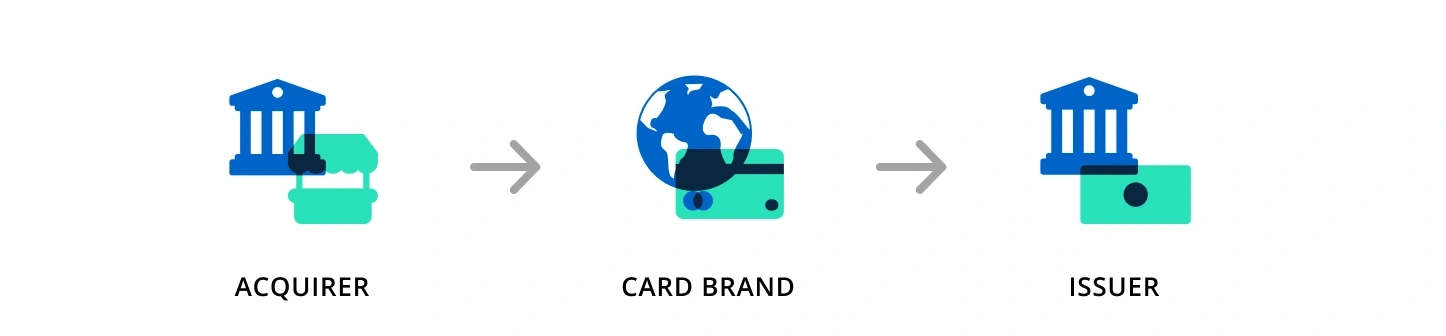

Once Jason clicks the purchase button, the payment gateway encrypts his information and submits an authorization request for $200 to the acquiring bank (usually through the payment processor).

From there, the acquirer submits the authorization request to the issuer via the card brand (in this case, Visa) to determine if the merchant approves or declines the transaction.

Authorization request

If the issuing bank were a person, it would be asking two main questions upon receipt of the transaction request:

- “Did the merchant supply all the relevant information?”

- “Does the cardholder have the funds or credit to cover this transaction?”

This is all happening electronically within fractions of a second.

Depending on the answers to these questions, the issuing bank then submits an authorization response. There are dozens of different authorization response codes, but they usually fall into two buckets: approval or decline.

Declined transactions

The most common reasons for a declined transaction are the following:

- Insufficient funds or credit to pay for the purchase

- The cardholder claimed a lost or stolen card, indicating a fraudulent charge

- A technological malfunction somewhere in the transaction pipeline

- Important information was entered incorrectly

Approved transactions

Merchants will receive an approved authorization response if both of the following are true:

- There is enough money in the account (or available credit) to pay for the purchase

- The card hasn’t been reported lost or stolen

Authorization response

Fortunately, Jason has plenty of credit still available and the issuer doesn’t see any reason why he can’t buy Kat’s guitar. So, the transaction is approved and advances to the next stage of the life cycle.

PHASE #3

Settlement

Kat is jazzed she made a sale. But there’s a problem. She doesn’t actually have Jason’s money in her merchant account yet.

Kat obviously needs the money in her account to cover the costs of running a music shop. So how does it get there?

Answer: settlement and funding.

Settlement is the process of Kat’s acquiring bank going out and acquiring the funds from Jason’s issuing bank.

Settlement

Since Jason owes Kat for the transaction, the issuing bank extends a line of credit to Jason for the $200 he’s promised. Then, the issuer passes on what’s owed — minus interchange fees for the bank’s services.

The issuing bank submits the payment to Visa. Because Visa provides infrastructure, network, and security, the brand is entitled to compensation. Visa takes its cut, and forwards the remainder of the money down the line to the acquiring bank. The acquirer and payment processor also have to be reimbursed for their processing costs, and sometimes a reserve account has to be funded.

Once everyone is paid — Visa, the acquirer, the processor, and sometimes the gateway — the money that’s left is settled in Kat’s merchant account.

Settlement

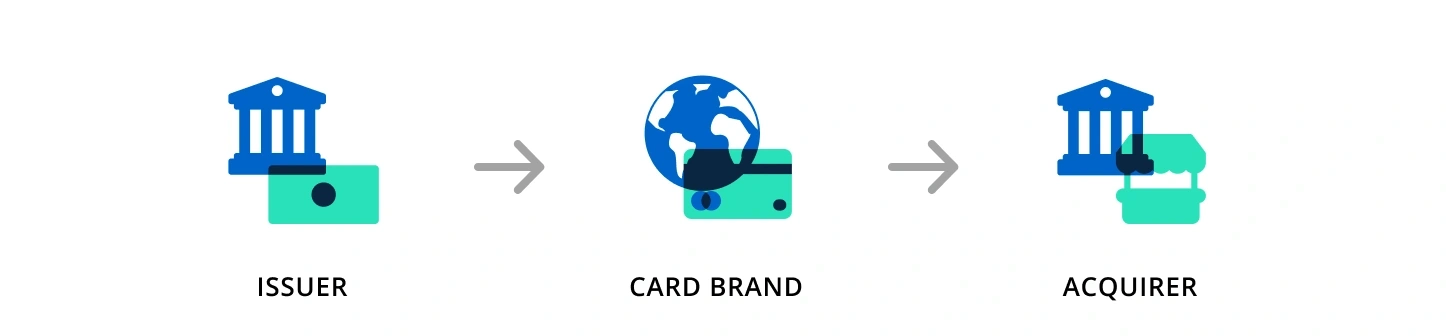

Once the money is handed off to Kat’s acquiring bank, the issuing bank turns around and tries to recoup those funds from Jason. In Jason’s situation, that’s done in the form of credit card debt (if Jason used a debit card, the bank would withdraw the funds from his account).

Repayment

Kat usually settles her transactions once a day. But sometimes, settlement for certain transactions isn’t as prompt. Kat often receives custom orders, and it takes a while to get the guitars ready. She doesn’t want to charge the card until the merchandise ships, but what if the customer’s account doesn’t have available funds when she’s ready to settle?

In these situations, Kat uses an authorization hold to freeze the money in her customer’s account until she is ready to move it to her own merchant account.

How Refunds Work

Most transactions finish at the settlement stage, but the lifecycle doesn’t always end there. Two additional workflows could unfold if the transaction doesn’t go as expected.

The first is a refund.

Refunds follow a similar process as transactions but in reverse.

When a customer requests a refund, the merchant sends a credit card authorization request to the issuer via the gateway. This authorization process checks to make sure the customer’s account is still open and can receive the funds.

Authorization request

The authorization request can either be approved or denied. If denied, the merchant will usually have to ask for a different card (from the same brand) or issue a store credit.

Authorization response

Once approved, the merchant settles the transaction with the acquirer (via the processor) and the card brand notifies the issuer that credit should be applied to the customer’s account.

Settlement

Refunds aren’t ideal. They cause you to lose money and can turn into a logistical nightmare to manage. But if you don’t issue a refund — either because it doesn’t align with your policies or the customer doesn’t give you the opportunity to make things right — the situation could take a turn for the worse.

Let’s go back to our example interaction between Kat and Jason to understand what could happen next.

Jason isn’t pleased with the guitar. He expected something different. Now, he wants his money back.

Unfortunately, Jason was a bit too hasty in his purchasing and didn’t pay attention to any of the disclaimers all over Kat’s site: “No refunds on used guitars.”

But Jason is determined to get his money back and will exercise every option at his disposal to do so — even a chargeback.

How Chargebacks Work

A chargeback, like a refund, is a transaction reversal. It reverses the original purchase by withdrawing funds that were deposited into your business’s bank account and returning them to the cardholder.

Unlike a refund, you have no control over repayment in a chargeback scenario. The entire conversation happens between your customer and the issuer.

Chargebacks often place businesses in precarious situations. Let’s look at the ripple effects of Jason’s chargeback decision in the following sequence of events.

PHASE #1

Chargeback

First, Jason tries to email Kat and personally ask for a refund. Kat kindly explains the reasoning behind her no-refund policy on used instruments and stands firm in her refusal to return the funds.

Unsatisfied by Kat’s response, Jason decides to dispute the charge with his issuing bank.

He contacts a representative from his issuing bank and claims Kat’s Music Shop is unreasonably refusing to refund his money after selling him a product.

Based on Jason’s claims, the representative decides the case warrants a chargeback.

The bank representative enters the relevant information into the Visa online portal and initiates the dispute. Once filed, the issuing bank credits the $200 back to Jason’s account.

At the same time, Visa forwards the chargeback to the acquiring bank. Kat’s merchant account is not only debited $200 but also dinged for a chargeback fee. The acquiring bank sends a chargeback notice to Kat, who’s shocked to discover the news.

Chargeback

At this point, Kat has two options: accept the chargeback and the loss of revenue or fight back and recover her money.

Armed with plenty of evidence and the confidence that she did nothing wrong, Kat decides to fight.

PHASE #2

Chargeback Response

Kat collects every shred of information on Jason’s transaction — an item description, a copy of the refund policy, his receipt, payment information, their email conversation, and more.

She writes a rebuttal letter explaining the situation and submits it to her acquiring bank. A representative at the acquiring bank evaluates the evidence and decides that it’s a compelling counter-argument. Kat’s account is credited with $200 revoked by the chargeback.

The bank’s representative then logs in to the Visa portal and submits a chargeback response. This chargeback response moves through the Visa network back to the issuing bank.

Chargeback response

At this point, Jason and his bank have an important decision to make.

Either the case is dropped and Jason accepts responsibility (which is what happens most of the time) or the fight rages on.

PHASE #3

Escalation

If Jason still decides to dispute the transaction, he can ask the issuing bank to challenge the transaction a second time (in official terms, this is called pre-arbitration).

If Kat still stands firm, Jason has the option to escalate the case beyond the scope of the chargeback process. He can ask Visa to intervene and make a final decision.

This process, called arbitration, is the courtroom equivalent of skipping a plea deal and taking a case straight to trial. The stakes are much higher and the fees are steep. The escalating party must be extremely confident in their ability to win. If their case is strong enough, they’ll end up with the money. But if they lose, there’s a risk they’ll need to pay all the fees (on top of the initial purchase amount).

At this point, the charge is in Visa’s court — literally.

The above workflow applies to the majority of chargebacks. However, there are certain situations where the process differs from the norm.

Be Prepared for Chargebacks

If you’re not yet receiving chargebacks, it is probably only a matter of time. While there are many practical ways businesses can prevent chargebacks, there’s no way to eliminate them altogether.

As your business grows, so will your need to minimize the financial impact of chargebacks. The more proactive you are, the more manageable the situation will be.

But if your chargeback situation becomes something you can no longer manage on your own, Kount can help. Sign up for a demo when you are ready to remove the complexities of payment disputes and protect your hard-earned revenue.